Many claim delays stem from insurance coordination issues, frustrating providers and slowing reimbursements. Coordination of Benefits (COB) is a frequent but often misunderstood billing challenge where multiple insurers determine who pays first. About 20-30% of multi-payer claims hit COB snags, per industry reports.

COB rules prevent duplicate payments when patients have dual coverage, like employer plans plus Medicare. Get it wrong, and claims bounce between payers, adding 30-90 days to collections. Front-desk verification misses and outdated patient data make it worse. Payers like BCBS or UnitedHealthcare often auto-deny until the primary EOB arrives.

Billing teams waste hours resubmitting, hurting AR days. Simple checks up front fix most issues. In this article, we’ll cover COB basics, how it works, common scenarios and pitfalls, delay causes, best practices, and support options to keep cash flow steady.

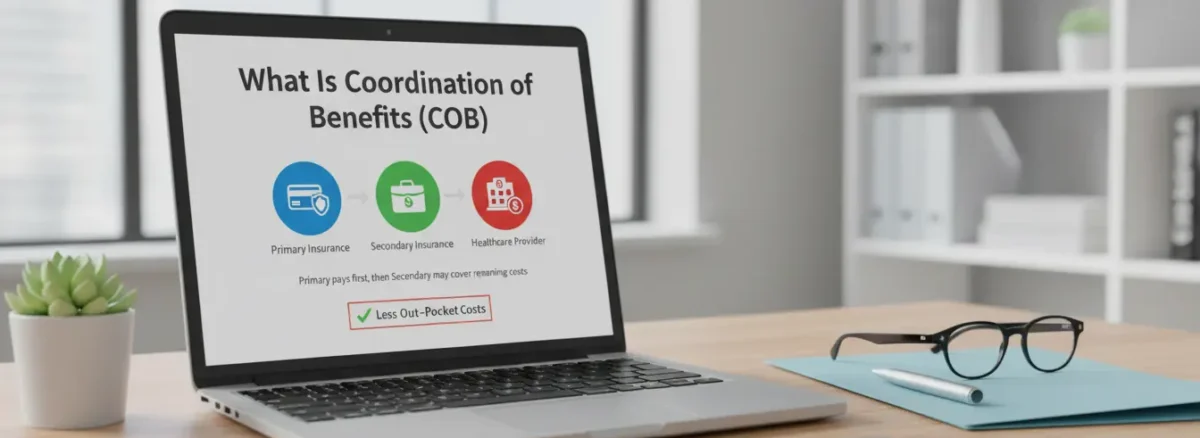

What Is Coordination of Benefits (COB)?

Coordination of Benefits (COB) is the process insurers use to decide payment order when a patient has multiple health plans, ensuring no overpayment. It applies to dual coverage like two employer plans, Medicare plus private insurance, or Medicaid as secondary.

COB exists to coordinate payouts correctly—the primary payer covers first, secondary picks up remaining eligible costs up to 100%. Without it, patients might get excess refunds, or providers face clawbacks.

This keeps healthcare affordable and claims clean, but requires accurate patient insurance details upfront.

How Coordination of Benefits Works

The primary payer covers claims first up to its allowed amount, issuing an Explanation of Benefits (EOB) that the secondary payer uses to determine remaining responsibility, capping total at 100%.

CMS mandates this for Medicare coordination, sharing eligibility data with other payers via the Benefits Coordination & Recovery Center (BCRC) for automatic crossover when agreements exist.

For working-age patients, employer group health plans (EGHP) are primary if the employer has 20+ employees; Medicare becomes secondary, flipping at retirement. The “birthday rule” applies to dependents: the parent’s plan with the earlier birth month pays primary.

Claims process: Verify order at intake, submit to primary via EDI 837 (with COB segments), receive EOB (14-45 days), attach to secondary claim. Industry data shows initial denial rates around 11-12% tied partly to COB errors like coordination of benefits denials.

Nearly 20% of all claims are denied initially, with up to 60% never resubmitted—COB mishandling contributes significantly, according to AHIMA reports. Over 12.4% of refused outpatient claims carry the CO-22 code due to COB issues

Why COB Causes Claim Delays

COB issues delay up to 20% of claims initially, per CMS and industry benchmarks, as payers enforce strict sequencing

Incorrect or Outdated Insurance Information: Patient details change frequently—new jobs or Medicare eligibility flips primary/secondary. Without updates, claims hit the wrong payer first, bouncing for 30-60 days; Experian reports this in 25-30% of denials

Claims Sent to Wrong Payer First: Skipping verification sends to secondary prematurely, triggering auto-denials. Kodiak data shows initial denial rates at 11.8%, rising with COB errors

Missing Primary Payer EOB: Secondaries require EOB proof; absence stalls 15-20% of cases, with AHIMA noting 60% of denied claims never resubmitted

Payers Verifying Responsibility: CMS BCRC audits add time, especially Medicare crossovers.

These inflate AR by 20-40 days on average.

Common COB Mistakes That Lead to Denials

COB errors account for a significant portion of claim denials, often 20-30% in practices with high dual-coverage patients, turning clean bills into rework.

These mistakes are preventable with checklists and training—here’s a detailed look at the most common ones, why they happen, and how to fix them.

Not Verifying Insurance at Each Visit

Rushed check-ins skip full eligibility runs, missing updates like a patient’s new job or Medicare activation. Result: Claims go to the wrong primary payer, denied with CO-22 codes.

This hits 25-35% of denials; solution: Mandate portal checks (e.g., Availity, Change Healthcare) for every appointment, confirming order with patient signatures.

Failing to Update COB Information

Patient data in your EHR doesn’t sync with life changes—spouse’s plan ends, child ages off policy. Payers reject mismatches during auto-edits. Impacts 20% of issues; fix by reviewing demographics at intake and annually, using secure patient portals for self-updates.

Submitting Claims Out of Sequence

Billing rushes secondary claims before primary EOB arrives, prompting immediate “premature” denials. Common in high-volume offices; adds 30-45 days of rework. Always sequence: primary first, wait 14-21 days for EOB, then secondary with attachment.

Documentation Gaps in Charts

Notes lack specifics like “accident—auto primary” or dual-plan details, leaving payers to guess responsibility. Appeals fail without proof; chart explicitly, e.g., “COB: Employer ABC primary per pt, Medicare secondary.”

Overlooking Revalidation or Group Changes

Corporate policy shifts or contract ends alter primacy unnoticed. Quarterly audits catch this, reducing surprises.

Best Practices to Prevent COB-Related Delays

Implementing solid COB habits can slash delays by 30-50%, turning chaotic billing into predictable revenue. Focus on verification, staff training, and tracking—these steps work for any practice size.

Verify Insurance and Coverage Order Upfront

At every patient visit, run real-time eligibility through payer portals or clearinghouses like Availity. Ask patients to confirm primary/secondary payers and note changes on intake forms. This catches 70-80% of order flips early, preventing downstream denials.

Educate Front-Desk and Billing Staff

Hold monthly trainings on COB rules, birthday rule for kids, employer vs. Medicare priority, and Medicaid as payer of last resort. Use real denied claims as examples and quiz staff—knowledge gaps cause 40% of errors.

Submit Claims in Correct Order

Bill the primary payer first via EDI 837 with full COB details. Wait for their EOB (set 21-day reminders), then attach it to secondary claims. Flag COB patients in your EHR for auto-holds.

Track and Follow Up on COB Claims

Use aging reports to monitor beyond 30 days; dedicate a staffer for weekly payer calls or portal chases. Appeal denials promptly with EOBs and notes—recovery rates hit 65% if acted on fast.

Leverage Tools and Audits

Adopt software like Waystar for auto-COB detection. Audit 10% of dual-coverage claims monthly to spot patterns.

How MedAce Healthcare Helps Manage COB Issues

MedAce Healthcare streamlines COB challenges with expert revenue cycle support, ensuring claims flow correctly from day one. The team handles insurance verification and COB checks for every patient, identifying primary/secondary orders upfront to prevent sequencing errors.

They manage claim sequencing and submission, billing primaries first, securing EOBs, and routing secondaries seamlessly—cutting delays by 40-60%. Payer follow-ups come standard, with dedicated reps chasing stalled claims and appealing denials using full documentation.

Clients enjoy reduced delays, faster payments (AR under 30 days), and higher clean claim rates. MedAce integrates with your EHR for real-time alerts, freeing staff for patient care.

FAQ

- What exactly is Coordination of Benefits (COB)?

Coordination of Benefits is a set of rules that insurance companies use when a person is covered by more than one health plan. It decides which insurance pays the bill first and which one pays second so that the total payment doesn’t exceed the actual cost of the service.

- How do I know which insurance pays first?

The “Primary” insurance pays first. Usually, if you have a job with insurance, that plan is primary. If you are retired, Medicare might be primary or secondary depending on your former employer’s size. For children covered by both parents, the “Birthday Rule” usually applies: the parent whose birthday falls earlier in the calendar year pays first.

- What happens if the wrong insurance is billed first?

If the claim goes to the secondary insurance before the primary one has paid, it will almost always be denied. This can delay your payment or the provider’s reimbursement by 30 to 90 days while the billing team has to start the process over from scratch.

- Why does my doctor’s office ask for my insurance info every time?

They ask because insurance status changes quickly—people change jobs, turn 65, or get married. Verifying your info at every visit prevents “COB denials,” which are one of the biggest reasons medical bills get stuck or rejected.

- Does having two insurance plans mean my healthcare is free?

Not necessarily. While having a secondary plan can help cover your deductibles or co-pays left over by the primary plan, it still depends on your specific coverage. The two plans “coordinate” to cover up to 100% of the “allowed amount,” but you may still owe a balance if neither plan covers a specific service.

- What is a “primary EOB” and why is it important?

An EOB (Explanation of Benefits) is a document from your first insurance showing what they paid and what they didn’t. The secondary insurance must see this document before they will pay their portion. Without the primary EOB, the secondary claim will be put on hold indefinitely.